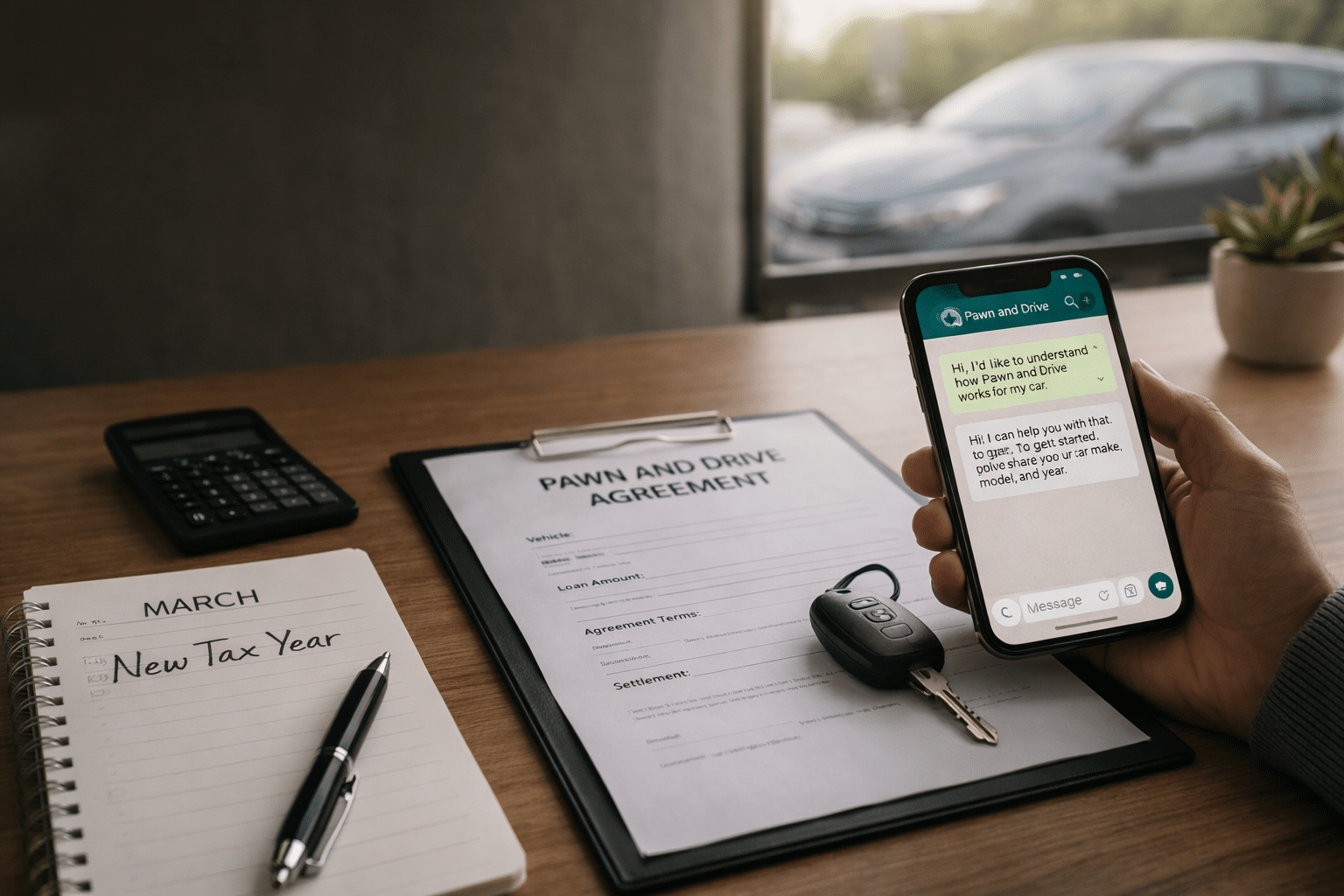

March often feels like a reset.

The new tax year starts. School and work routines settle down. After the pressure of February, many people want to get control of their cash flow and avoid carrying the same stress into the rest of the year.

That is where a common question comes in.

Can I use my car to get short-term cash flow without selling it?

The short answer is yes, in some cases.

Pawn and drive is one option people use when they need short-term financial support but still need their car for work, family, or daily life. This article explains how it works, when it may make sense, and what to check before agreeing to anything.

Why people look for short-term cash flow support in March

March is different from February.

In February, the pressure is often immediate. In March, people are more likely to step back and look for a practical way to stabilise things.

That may mean:

- catching up on bills

- covering school or household expenses

- managing a temporary gap in cash flow

- avoiding a rushed decision, like selling a useful asset

For many people, a car is too important to lose. It helps them get to work, transport family, run errands, or support a business. Selling it may solve one problem quickly, but it can create another just as fast.

That is why some people look at ways to borrow against the value of a car while still driving it.

What is pawn and drive?

Pawn and drive is a type of asset-based finance.

In simple terms, it allows you to use your car as security for a short-term agreement. You receive funds based mainly on the vehicle’s value, and you continue driving the car while repaying under agreed terms.

This means:

- you do not need to sell your car

- the agreement is based mainly on the vehicle’s value

- it is meant for short-term support, not long-term financial planning

This is different from simply selling the car for cash. It is also different from some traditional loans, where approval depends heavily on credit profile and longer application processes.

How pawn and drive works

The process is usually straightforward.

1. Your car is assessed

The provider looks at factors such as:

- age

- mileage

- overall condition

- paperwork

- market value

2. An amount is offered

The amount offered is based mainly on the car itself, not only on your credit profile.

3. The agreement is explained

If the option suits you, the terms should be explained clearly and put in writing.

4. You receive funds

Once everything is in order, you receive the agreed amount.

5. You keep driving your car

This is one of the main reasons people choose pawn and drive instead of selling.

6. You repay over the agreed period

When the agreement is settled, it ends.

Why this can make sense at the start of the tax year

March is often when people want a better plan, not just quick relief.

Using your car as short-term financial support can make sense when:

- the pressure is real, but temporary

- you want to keep your transport

- you need breathing room without making a permanent decision

- you want a more direct option than a traditional loan process

For some people, this feels more controlled than selling a car or taking on long-term debt for a short-term problem.

That does not mean it is always the right choice. It means it can be worth understanding properly before dismissing it or rushing into something else.

Why people choose this instead of selling their car

Selling a car can bring in money quickly, but it comes with trade-offs.

Once the car is gone, daily life often becomes harder. Getting to work costs more. School runs become more difficult. Business owners may lose flexibility. Buying another car later can also be more expensive than expected.

Pawn and drive appeals to people who want to unlock some of the value in their car without giving it up completely.

That is often the biggest difference:

- selling gives immediate cash, but you lose the vehicle

- Pawn and Drive gives short-term support while you keep using it

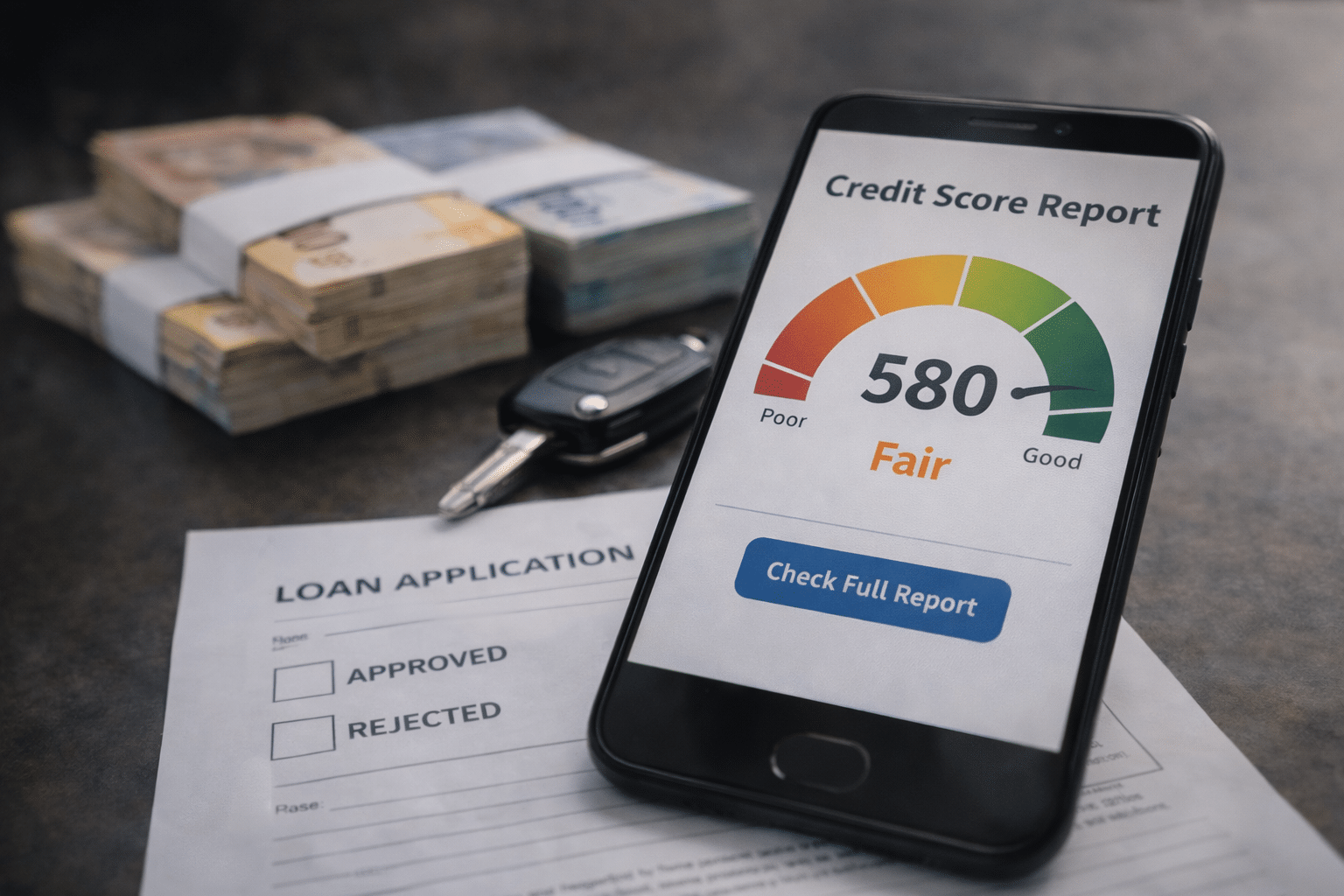

Does credit score matter?

One of the reasons people ask about pawn and drive is that traditional borrowing can be difficult.

Banks and other lenders often rely heavily on credit checks, affordability rules, and longer approval processes. With pawn and drive, the value of the vehicle plays a much bigger role.

That said, the important point is not just whether you qualify.

The more important question is whether the agreement is clear, manageable, and suited to your situation.

A short-term financial tool should help you stabilise things, not create extra pressure later.

What affects how much you may get?

There is no fixed amount that applies to everyone.

The amount depends on practical factors such as:

- vehicle age

- mileage

- condition

- service history or paperwork

- current market value

Before speaking to any provider, it helps to have a realistic idea of what your car is worth. That gives you more confidence and makes it easier to judge whether the conversation is reasonable.

Clarity matters more than chasing the highest number.

You should understand:

- how repayment works

- what settlement looks like

- what happens if your circumstances change

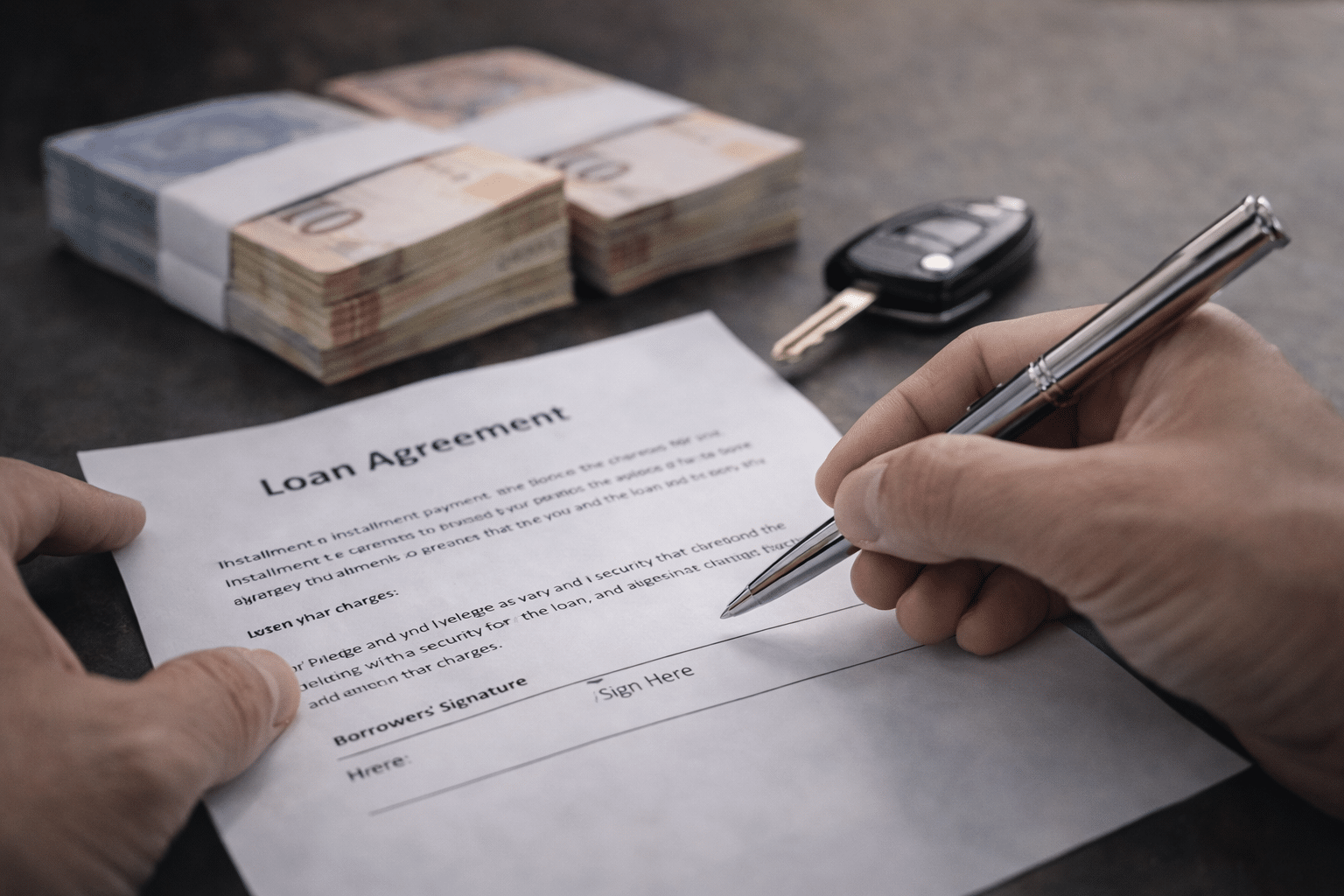

What to check before signing anything

This part matters.

If you are considering pawn and drive, make sure the provider:

- explains the agreement in plain language

- puts the terms in writing

- gives you time to ask questions

- explains repayment and settlement clearly

- does not pressure you to sign immediately

If something feels rushed or vague, pause.

A legitimate provider should be willing to explain the process properly. Understanding the agreement matters more than speed.

When pawn and drive may be a good fit

Pawn and drive can make sense if:

- you own your car

- you need short-term cash flow support

- you still need the car for everyday life

- you want to avoid selling a useful asset

It may not be the right fit if:

- you need a long-term borrowing solution

- you are unsure how repayment would work

- another option would suit your situation better

That is why the first step should be understanding, not committing.

What usually happens next

If you want to explore the option, the next step is usually simple.

- You share basic details about your car

- The process and possible options are explained

- You decide whether it makes sense for you

No pressure. No obligation to continue.

Sometimes that clarity is enough to help you make a better financial decision for the months ahead.

Final thought

If you are trying to start the new tax year on a stronger footing, the goal is not just to solve today’s pressure. It is to do it in a way that protects your mobility and supports the rest of the year.

For some people, pawn and drive offers that balance.

It is not about giving up your car. It is about understanding whether the value in it can help you create breathing room while keeping life moving.